Last week was rough for the big tech firms, with almost $1 trillion wiped off the value of the biggest companies. But don’t worry – we’re here to help you understand it.

Five of the largest tech companies, who now go by the acronym MAMAA (Meta (formerly Facebook), Apple, Microsoft, Amazon, and Alphabet), reported their Q3 2022 earnings last week. After they reported their results, the companies saw their share price fall an average of 10%. Here’s a rundown of what happened.

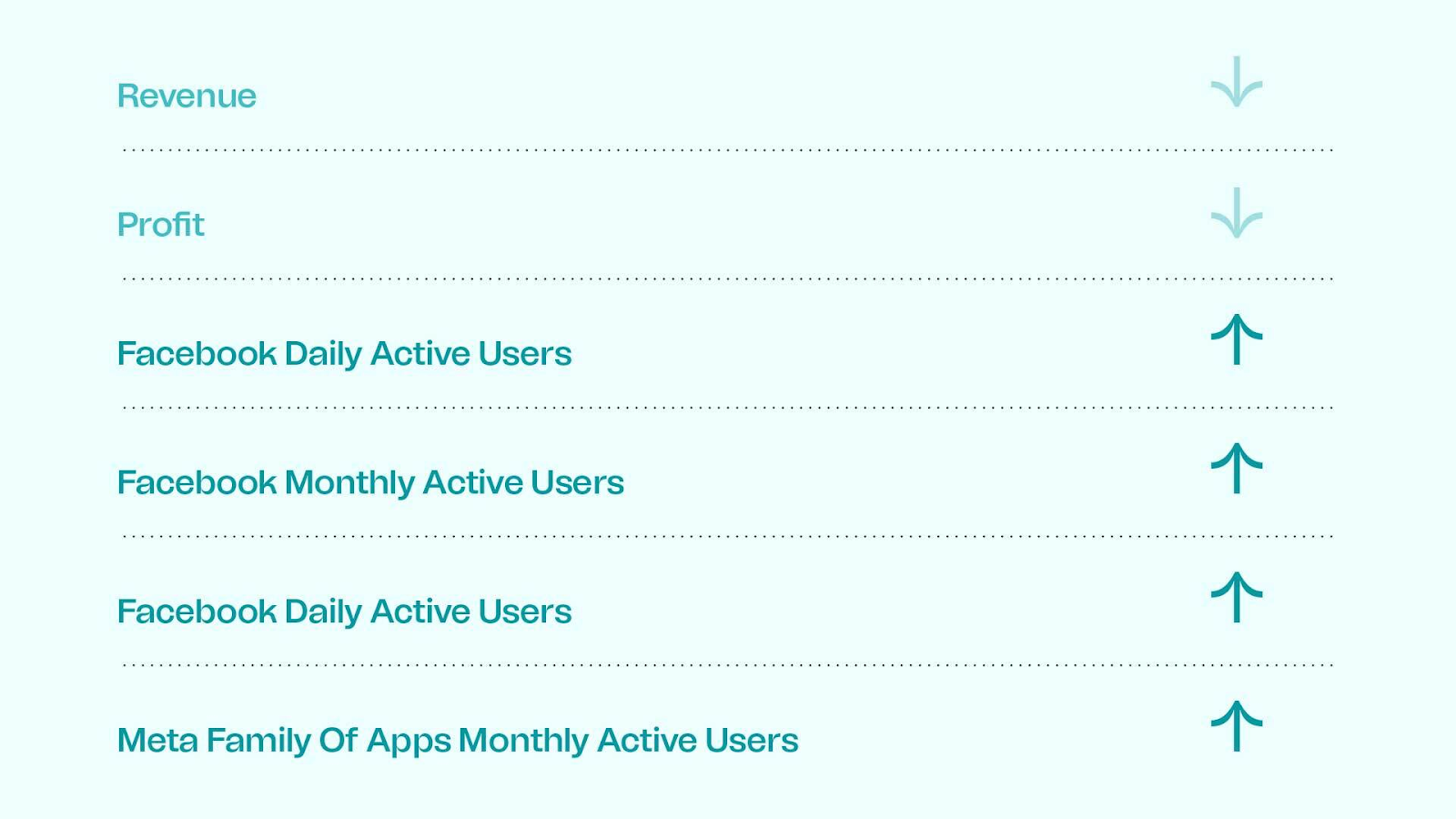

It started with Meta.

Meta reported revenue of $27.7bn which was 4% lower than 2nd quarter revenues but 1.15% higher than Wall Street expected. Though revenue was higher than anticipated, quarterly profit fell by over 30%.

Facebook’s daily active users rose by 3% to 1.98 billion, above an expected 1.86 billion, and monthly active users grew 2% to 2.96 billion (slightly lower than expectations of 2.97 billion).

The Meta “Family of Apps” (Facebook, Instagram, and WhatsApp) saw daily , and monthly active people rise by 4% each to 2.93 billion and 3.71 billion, respectively. Ad impressions across the family rose 17%, but the average price per ad fell by 18%. So while more people were clicking on ads, the revenue per ad fell.

Overall, it was a mixed bag of results. However, after they reported earnings, Meta shares fell by almost 25%, wiping out $84.6bn from the company’s market value. This left Meta’s shares 74% below the all-time high it reached just 14 months ago.

\

Why such a harsh reaction?

Investors’ big issue with Meta was their spending budget for next year. Meta said they plan to spend up to $39 billion on capital expenditure and $101 billion on operational costs next year, which is way higher than the $34 and $87B they expect to spend on both line items this year.

That is a huge jump in expenses for Meta, especially in 2023, when most investors expect a recession. Also, Meta expects Reality Labs (the part of Meta behind the Metaverse) to lose more money in 2023 than in 2022.

Most organisations are looking to cut down on spending in 2023, while Meta is looking to spend more, even though the additional spending isn’t likely to boost revenues.

A few days before Meta announced its results, a long-term investor wrote an open letter to Mark Zuckerberg and Meta’s board of directors, saying, “Meta has drifted into the land of excess — having too many people, too many ideas, too little urgency. This lack of focus and fitness is obscured when growth is easy but deadly when growth slows and technology changes”.

This shareholder, Brad Gerstner, CEO of Altimeter Capital, recommended that Meta reduce employee expense (operating) by $5bn, reduce capital expenditure by $5bn, and cap metaverse investment to not more than $10bn.

This quarterly earnings report shows that Mark plans to do the opposite of what Brad recommended by spending over $10bn more on operating expenses and $5bn more on capital expenses (which could include the metaverse).

And because of the nature of Meta’s share structure, only Mark Zuckerberg has the final say on the company’s direction. Thus, the only option for shareholders is to stay on board or sell their shares. Hence, the broad sell-off.

Then came Alphabet and Microsoft

Alphabet

Alphabet missed both top-line and bottom-line expectations. Revenue grew slower than Wall Street expected, and earnings per share were also 15% lower than expected. YouTube saw ad revenue fall for the first time since it reported financial performance separately in 2020.

The outcome: Alphabet’s share price fell 6.6% after they reported earnings.

CEO Sundar Pichai said, “Google is pushing to become more efficient by aligning resources to invest in their biggest growth opportunities, and employee additions in Q4 will be significantly lower than Q3”. At least one CEO is being prudent after reporting disappointing numbers. Side eye Meta.

Microsoft

Microsoft has a mixed bag of results. Cloud services revenue of $20.3bn was 20% higher than what it was in the same period in 2021, which was good news for all who saw Microsoft’s cloud service, Azure, as the winning player in the cloud space. However, its computer weakness exposed businesses, and the dollar’s strength affected revenue and profits.

Like Meta, Microsoft’s forward-looking statements were the main worry for investors. Microsoft says it expects a 5% slowdown in Azure, whereas Wall Street was expecting a 3% slowdown.

Also, Alphabet stained Microsoft’s white when discussing GCP (Google Cloud Platform). Google alluded to the challenging macro environment (inflation, rising interest rates, and recession fears) affecting their cloud business.

Microsoft’s share price fell 6.7% after its financial results came out.

Finally, Amazon and Apple

Amazon

Amazon saw its share price fall almost 13% in after-hours trading on Thursday night after it missed revenue expectations. It gave weak forecasts for its all-important holiday fourth-quarter sales. Amazon indicated that Q4 2022 revenue could be as much as $15bn lower than the $155bn Wall Street was expecting.

Amazon’s AWS reported that growth was slowing faster than expected. Similar to what Google and Microsoft said about their cloud businesses.

Apple

Only Apple managed not to disappoint, reporting revenue and profits above Wall Street’s expectations. They reported their highest-ever quarterly revenue of $90.1 billion and reached a new record for the number of active Apple devices in circulation. Macs sold at a record pace in Q3 2022, which covered up for lower-than-expected iPhone sales. Apple’s share price was initially down 4% after they reported their financial results.

After Meta, Microsoft, Amazon, and Alphabet reported their financial report, their stocks lost about $950bn in market value compared to before earnings. Apple’s good performance brought some profit for the MAMAA team, reducing the overall loss to $770bn in market value.

We can draw two main lessons from big tech earnings reports:

- A strong dollar is bad for global businesses that report their results in the dollar. This is because they have to convert their non-dollar earnings to dollars at a less favourable rate, making their dollar earnings look weaker.

- It also challenges the belief that the market has bottomed. If earnings continue to be lower than expectations, stock prices could fall further.